On Thursday, President Donald Trump signed a sweeping executive order that ordered federal banking regulators to investigate and punish financial institutions that deny services to individuals or businesses based on their political or religious beliefs. According to a report by The New York Times, the order, which represents one of the strongest executive moves of Trump’s second term, follows developing claims from conservative groups and industries such as cryptocurrency that they have been victims of unfair debanking practices.

Confirmed by a White House release, the executive action directs that agencies, including the Federal Reserve, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation, examine both current and historical banking methods. The order asks these regulators to identify any cases where political, religious, or lawful business activities were a factor in denying service, with referrals to the Department of Justice required within 120 days for possible civil or criminal penalties.

Regulators Instructed to Act on Violations Within Set Timelines

According to the executive order, regulators must assess their supervised banks within 180 days to ensure adherence with anti-discrimination standards. Agencies have also been told to remove internal guidance that considers reputational risk, a rule once used by regulators to oppose banking dealings with clients seen as unsafe.

The removal of this practice marks a change in federal control, as banks had long complained that the reputational risk demands were unclear. Institutions said the law allowed regulators to limit services to clients not based on assessed financial risk but on expected concerns. In addition to targeting political and religious views, the order also addresses concerns raised by cryptocurrency companies and firearms manufacturers.

These industries have repeatedly claimed that they were denied banking access without clear justification. The order mandates that the Small Business Administration work with regulated financial institutions to identify and potentially reinstate any clients affected by “politicized or unlawful” service denials. It also requires regulators to purge any policies that may prevent banks from engaging with lawful businesses solely based on their industry category.

Personal Allegations by Trump Spark Renewed Interest in Issue

In a CNBC interview earlier this week, Trump claimed that major U.S. banks had denied him banking services following his first term. He said that JPMorgan Chase and Bank of America turned away substantial cash deposits and gave short notice for the closure of his accounts.

“I had hundreds of millions, many accounts loaded with cash. They said, ‘You have 20 days to leave.’” Trump Stated.

Neither bank confirmed the claims. JPMorgan said it does not close accounts for political reasons. Bank of America did not comment on specific client issues but welcomed clearer regulatory guidance. Major financial institutions have maintained that they do not deny service based on political or religious affiliations. Banks stated that account closures typically relate to financial risk factors such as money laundering, fraud concerns, or solvency issues.

However, banks have acknowledged that regulatory overreach may have influenced service decisions. In a joint statement, the Bank Policy Institute, American Bankers Association, Consumer Bankers Association, and Financial Services Forum expressed support for eliminating unclear regulatory guidance. They stated that regulatory discretion and complex rulebooks have made it difficult to serve all customers equally.

Alleged Government Involvement in Post-January 6 Account Closures

Trump’s executive order also references actions taken by banks following the January 6, 2021, attack on the U.S. Capitol. The order accuses financial institutions of participating in surveillance efforts against conservatives during that period. One ongoing lawsuit involves the Trump Organization’s case against Capital One.

The Trump family business claims the bank wrongfully closed its accounts after the Capitol riot. Capital One has denied any wrongdoing, and dispute continues. The move to eliminate reputational risk evaluations in bank supervision began earlier this year.

All three major federal banking regulators had already announced plans to withdraw from using this subjective standard. Trump’s order formalizes that process and ensures it applies across all relevant agencies. Banks had argued the reputational risk standard lacked clarity and enabled regulators to penalize lawful activities that could result in negative media attention.

Crypto Sector Included in Expanded Retirement Investment Order

Alongside the debanking order, Trump also signed a separate order on Thursday that expands access to alternative investments within retirement plans. The directive permits 401(k) investors to include digital assets such as cryptocurrency, real estate, and private equity in their portfolios.

The Blockchain Association welcomed both orders. The group stated that the elimination of debanking practices and expanded investment access would help lawful crypto businesses and consumers alike. The group described the orders as a signal that reputation-based banking restrictions would no longer limit access for lawful industries.

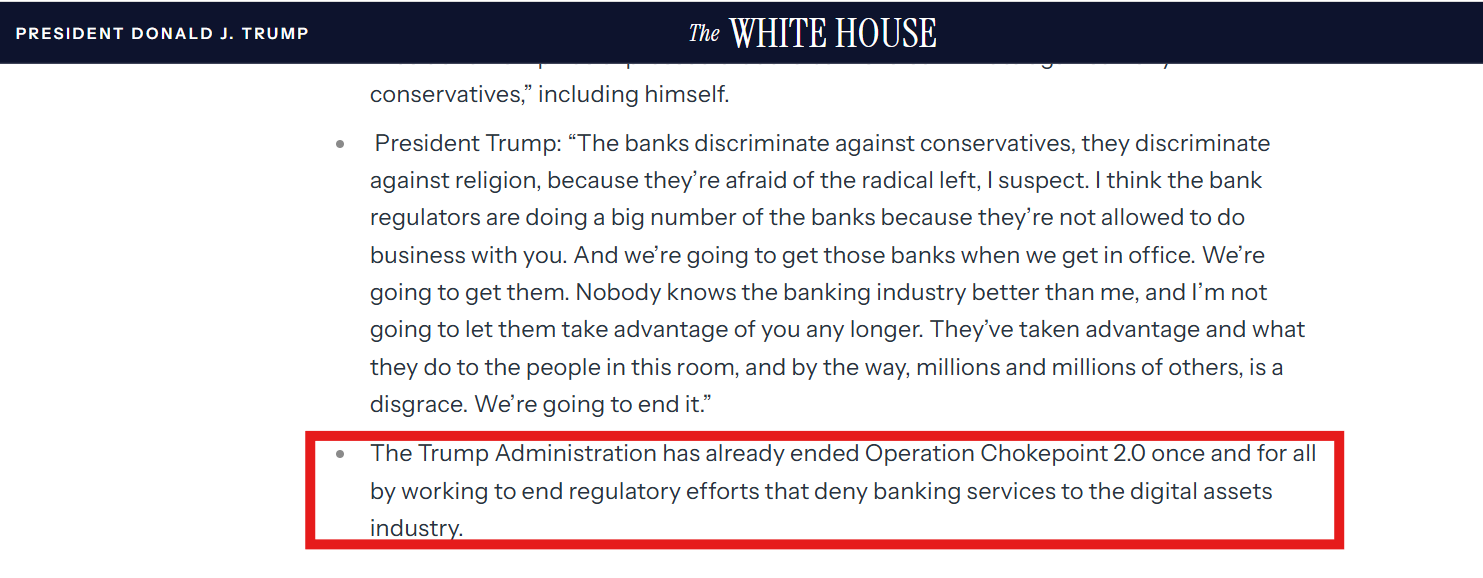

The issue of debanking has been linked to Operation Choke Point, an Obama-era policy that discouraged banks from doing business with high-risk industries. While initially aimed at curbing fraud and financial crime, Operation Choke Point was criticized for pushing banks to cut ties with lawful businesses such as firearms dealers and payday lenders.

Source: White House Fact Sheet

Although the program was officially ended during Trump’s first term, its influence on banking practices and regulatory culture has remained a point of contention among industry groups and conservative lawmakers.

Financial Industry Awaits Clarity on Implementation

While the executive order sets deadlines and outlines regulation processes, many in the financial sector are awaiting guidance on how regulators will apply the new rules. Questions remain about the demands that will be used to determine whether an account closure qualifies as unlawful debanking.

Legal experts noted that banks already have adherence procedures that measure risk based on anti-money laundering laws and financial health. The order now adds a layer of oversight related to belief-based discrimination, potentially requiring policy updates across the industry.

The White House said Thursday that such debanking practices erode public trust, freeze payrolls, and place financial strain on lawful citizens.

Officials provided examples of alleged service denials based on transactions involving terms like “Trump” or “MAGA,” or legal purchases at gun shops. Federal agencies now face clear deadlines to implement the executive order’s directives. Regulators have been ordered to assess their policies, complete reviews, and initiate any necessary disciplinary actions against banks that engaged in belief-based discrimination.